Advanced NT8 Market Microstructure Algo: Volumetric Quant Strategy (C#)

This product provides the complete, unlocked C# source code for an advanced quantitative algorithmic trading strategy built for NinjaTrader 8. Based on an enhanced Eisler-style event-impact model, this script is engineered for 1-minute Volumetric bars (Order Flow+) on the NQ and utilizes deep micro-structural market concepts.

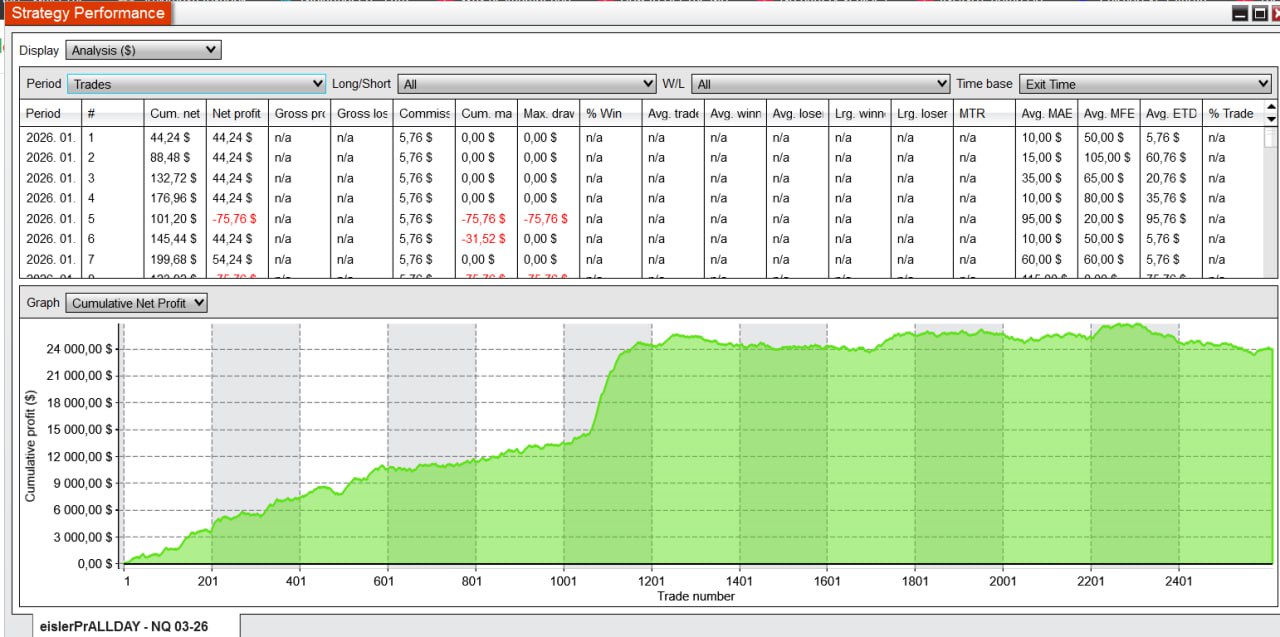

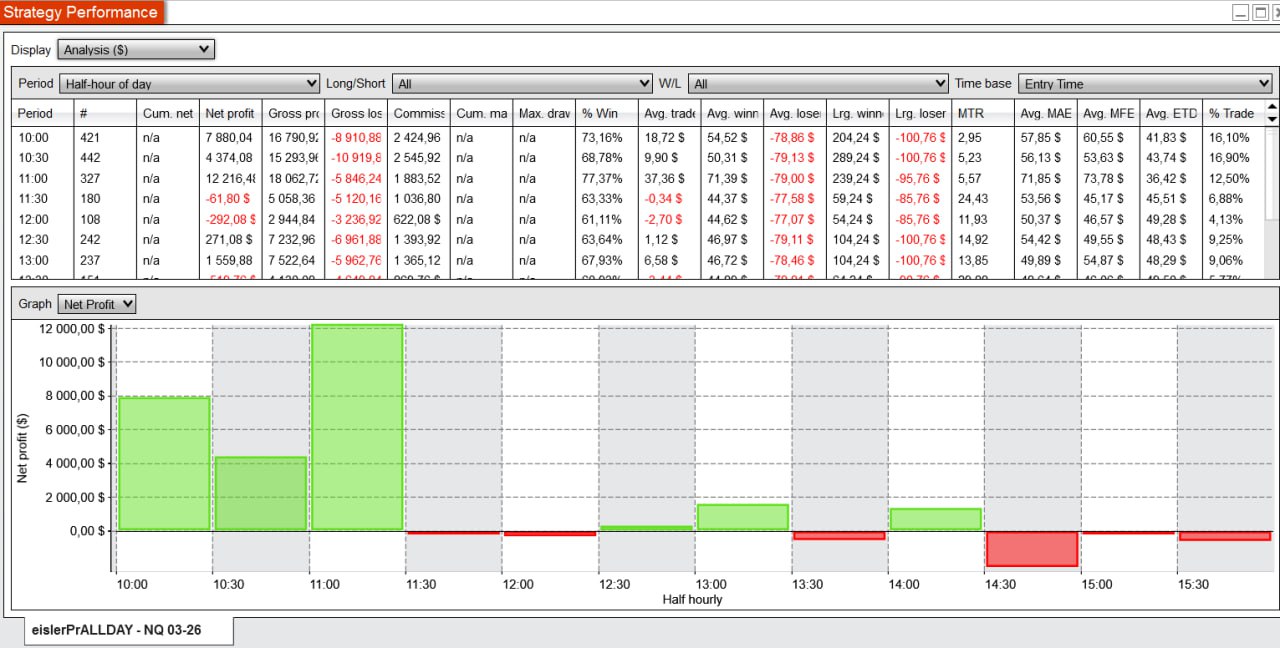

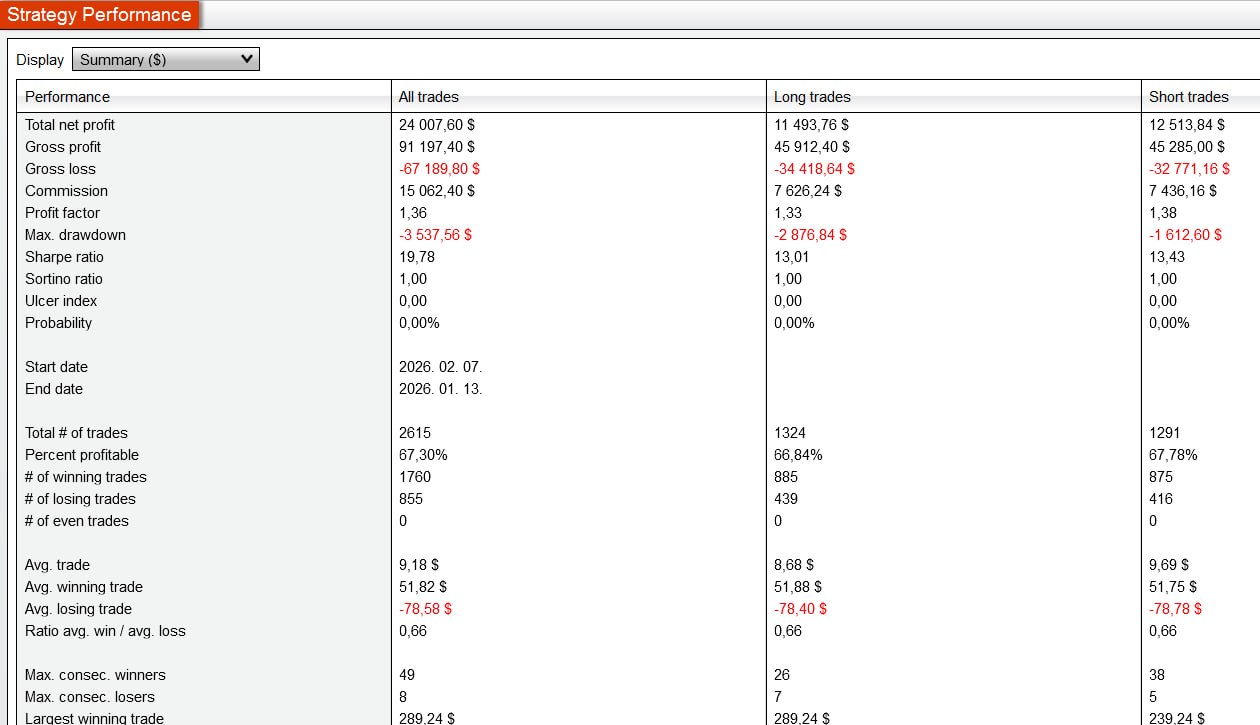

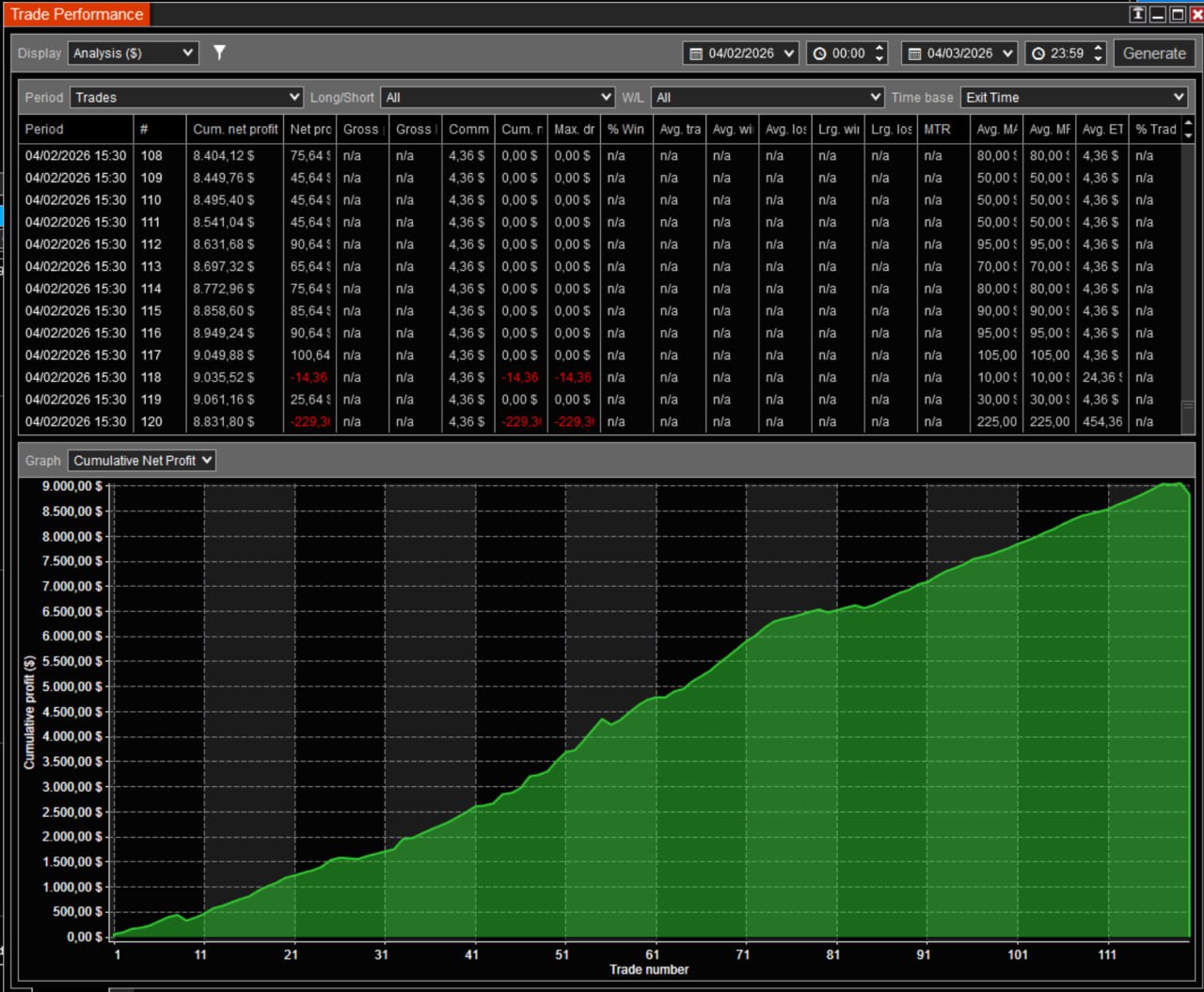

Important Disclaimer on Live Performance & Backtest Outliers Transparency is key. This strategy was rigorously tested using the NT8 Strategy Analyzer with Market Tick Replay, operating in an environment with absolute zero millisecond (0 ms) jitter. While the logic shows theoretical profitability between the hours of 9:30 and 11:30, the backtest results contain known outliers—specific trades that show a higher profit capture than is realistically possible due to perfect simulated fills.

In a live, real-world trading environment, the results are currently not positive. Natural market latency, routing delays, and live data jitter erode the micro-structural edge this specific logic relies on.

The Real Value: A Masterclass in Quant Architecture Do not purchase this expecting a plug-and-play, profitable trading bot. Buy this for the architecture. If you are a quant developer, a C# programmer, or a researcher building your own algorithmic systems, this code structure is an absolute goldmine. It provides a robust, highly organized foundation for building professional-grade quant strategies that handle real-world data issues.

Core Trading Mechanics & Window

Optimized Trading Window: Defaults to 9:50 AM – 11:30 AM, allowing the initial market open volatility to settle before the logic engages.

5-Minute Buffer Resets: Specifically tuned for the NQ, the strategy features a built-in periodic reset that flushes and cleans the internal arrays, buffers, and state machine every 5 minutes.

Level-II Independence: Computes market impact without needing a heavy

OnMarketDepth()subscription, relying entirely on L1 Bid/Ask/Last and Volumetric bar aggregates.Regime Switching & Sizing: Automatically adapts between large-tick and small-tick environments, and implements concave, impact-based position sizing scaled to an internal market activity proxy.

Advanced Latency & Jitter Protection Suite

The standout value of this code lies in its custom handling of imperfect live data feeds. It includes highly valuable proxy code to estimate data arrival jitter and protect the algorithm from bad execution.

Automatic Latency/Jitter Measurement: Uses a built-in proxy to measure inter-arrival times dynamically.

Staleness Gate: If the measured milliseconds become too high (stale quotes), the algorithm actively blocks new entries.

Jitter Gate (p95 Inter-Arrival): If the 95th percentile of inter-arrival time is too high, entries are blocked. This specifically protects the system when feeds like CQG become “lumpy” due to micro-bursts, buffering, or high system load.

Dynamic Tightening: Automatically tightens the entry threshold and limit offset calculations based on the real-time latency environment.

Signal Confirmation: Requires jitter-robust multi-tick confirmation before allowing a signal to fire, preventing false positives from delayed data packets.

Latency-Aware Order Handling: Manages orders with strict hold times and automatic expiration/cancellation if the market moves away or the order works for too long.

The Theoretical Foundation: Event-Impact & Market Microstructure

The strategy’s architecture is directly derived from the academic study “The price impact of order book events: market orders, limit orders and cancellations” by Zoltán Eisler, Jean-Philippe Bouchaud, and Julien Kockelkoren. This research explores how various order book events—not just market orders, but also limit orders and cancellations affect the future price changes of an asset. The C# code translates these concepts into a real-time trading algorithm. Below are the key mathematical models from the paper that form the backbone of the strategy’s logic:

1. The Transient Impact Model (Propagator Model)

The foundation of the algorithm relies on the idea that the mid-point price ($p_t$) at a given time is a linear superposition of the impact of past trades:

![]()

2. History Dependence & The “Dressed” Propagator

In real markets, events like limit orders and cancellations “dress” the impact of market orders. The model extends the price dynamics to include multiple hidden event types:

![]()

The strategy code utilizes an autoregressive adaptation of this concept to predict future price changes based on the aggregate order flow history, rather than treating market orders in isolation.

3. Gap Dynamics & Linear Fluctuations (Small-Tick Assets)

For small-tick assets (like the NQ), the “bare impact” of an event is not permanent; it depends heavily on the internal fluctuations of the order book gaps. The study models this using a Vector Autoregression (VAR) approach on past order flow:

![]()

This specific formula is mathematically mirrored in the strategy’s Recursive Least Squares (RLS) feature set and gap-flex correction states, allowing the algorithm to dynamically adapt to shifting liquidity conditions.

Important Notice

This product is a trading analysis tool, and therefore we do not take responsibility for any trading losses incurred while using it. Additionally, this product is non-refundable, so please ensure it meets your needs before making a purchase.

Lifetime License & Unlimited Installations

The NinjaTrader 8 Footprint Indicator comes with a lifetime license, allowing users to install it on an unlimited number of devices. This flexibility enables traders to access their customized order-flow analysis across all of their trading setups.

Reviews

There are no reviews yet.